What is an EDI e-Invoice ?

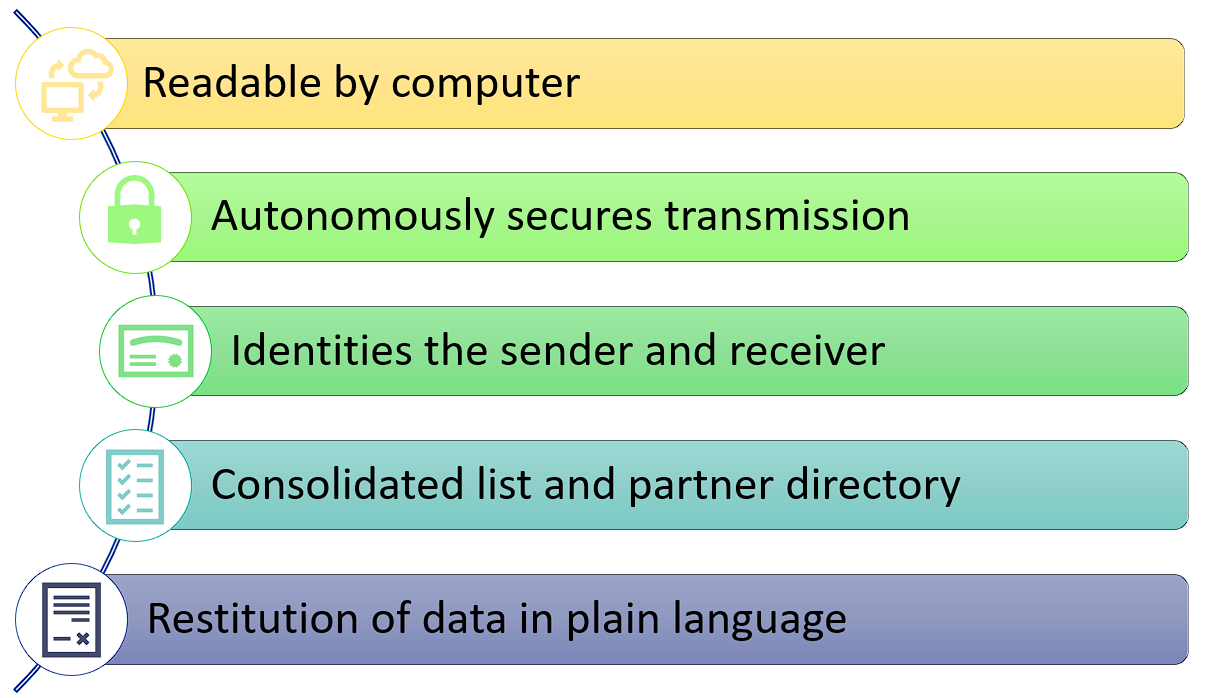

Invoices transmitted by Electronic Data Interchange (EDI) are in the form of a structured message, according to an agreed standard, allowing for reading by computer and which can be processed automatically.

They are de facto original invoices.

Electronic data interchange makes it possible to secure the transmission of electronic invoices autonomously, it alone guarantees the authenticity of their origin, the integrity of their content and their legibility.

For this purpose, the remote transmission system used must comply with the following conditions:

- The identity of the message sent and received.

- Creation of a summary list and a file of partners.

- Data archiving (see article BOI-CF-COM-10-10-30-10).

- Restitution of data in plain language (see BOI-CF-COM-10-10-30-10 as well).

NB : The summary list and the directory of partners are essential features of EDI.